分析:评估与结果分析

介绍

Analysis 旨在展示 日内交易 的图形报告,帮助用户直观地评估和分析投资组合。以下是一些可查看的图形:

- 分析位置

报告图

得分 IC 图

累计收益图

风险分析图

排名标签图

- 分析模型

模型性能图

Qlib中所有累积利润指标(例如收益、最大回撤)通过求和计算。这避免了指标或图表随着时间的推移而呈指数偏斜。

图形报告

用户可以运行以下代码以获取所有支持的报告。

>> import qlib.contrib.report as qcr

>> print(qcr.GRAPH_NAME_LIST)

['analysis_position.report_graph', 'analysis_position.score_ic_graph', 'analysis_position.cumulative_return_graph', 'analysis_position.risk_analysis_graph', 'analysis_position.rank_label_graph', 'analysis_model.model_performance_graph']

备注

有关更多详细信息,请参阅函数文档:类似于 help(qcr.analysis_position.report_graph)

用法与示例

analysis_position.report 的用法

API

- qlib.contrib.report.analysis_position.report.report_graph(report_df: DataFrame, show_notebook: bool = True) [<class 'list'>, <class 'tuple'>]

显示回测报告

示例:

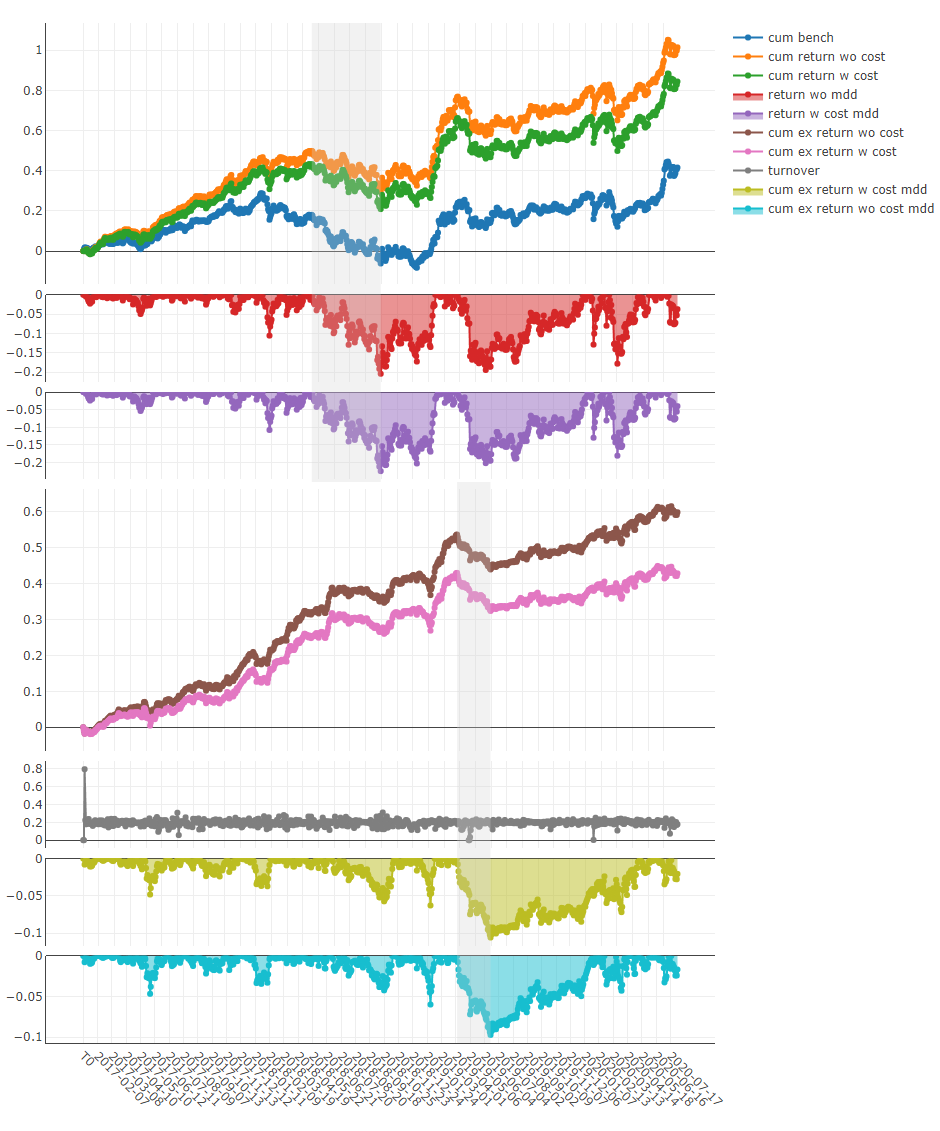

import qlib import pandas as pd from qlib.utils.time import Freq from qlib.utils import flatten_dict from qlib.backtest import backtest, executor from qlib.contrib.evaluate import risk_analysis from qlib.contrib.strategy import TopkDropoutStrategy # init qlib qlib.init(provider_uri=<qlib data dir>) CSI300_BENCH = "SH000300" FREQ = "day" STRATEGY_CONFIG = { "topk": 50, "n_drop": 5, # pred_score, pd.Series "signal": pred_score, } EXECUTOR_CONFIG = { "time_per_step": "day", "generate_portfolio_metrics": True, } backtest_config = { "start_time": "2017-01-01", "end_time": "2020-08-01", "account": 100000000, "benchmark": CSI300_BENCH, "exchange_kwargs": { "freq": FREQ, "limit_threshold": 0.095, "deal_price": "close", "open_cost": 0.0005, "close_cost": 0.0015, "min_cost": 5, }, } # strategy object strategy_obj = TopkDropoutStrategy(**STRATEGY_CONFIG) # executor object executor_obj = executor.SimulatorExecutor(**EXECUTOR_CONFIG) # backtest portfolio_metric_dict, indicator_dict = backtest(executor=executor_obj, strategy=strategy_obj, **backtest_config) analysis_freq = "{0}{1}".format(*Freq.parse(FREQ)) # backtest info report_normal_df, positions_normal = portfolio_metric_dict.get(analysis_freq) qcr.analysis_position.report_graph(report_normal_df)

- 参数:

report_df -- df.index.name 必须是 date,df.columns 必须包含 return,turnover,cost,bench。 .. code-block:: python return cost bench turnover date 2017-01-04 0.003421 0.000864 0.011693 0.576325 2017-01-05 0.000508 0.000447 0.000721 0.227882 2017-01-06 -0.003321 0.000212 -0.004322 0.102765 2017-01-09 0.006753 0.000212 0.006874 0.105864 2017-01-10 -0.000416 0.000440 -0.003350 0.208396

show_notebook -- 是否在笔记本中显示图形,默认值为 True。

- 返回:

如果 show_notebook 为 True,则在笔记本中显示;否则返回 plotly.graph_objs.Figure 列表。

图形结果

备注

X轴:交易日

- Y轴:

- cum bench

基准的累积收益系列

- cum return wo cost

不含成本的投资组合累积收益系列

- cum return w cost

含成本的投资组合累积收益系列

- return wo mdd

不含成本的累积收益的最大回撤系列

- return w cost mdd:

包含成本的累计收益的最大回撤系列

- cum ex return wo cost

与基准相比的投资组合的`CAR`(累计异常收益)系列,不包含成本。

- cum ex return w cost

与基准相比的投资组合的`CAR`(累计异常收益)系列,包含成本。

- turnover

换手率系列

- cum ex return wo cost mdd

不包含成本的`CAR`(累计异常收益)回撤系列

- cum ex return w cost mdd

包含成本的`CAR`(累计异常收益)回撤系列

上方阴影部分:对应于`cum return wo cost`的最大回撤

下方阴影部分:对应于`cum ex return wo cost`的最大回撤

`analysis_position.score_ic`的使用

API

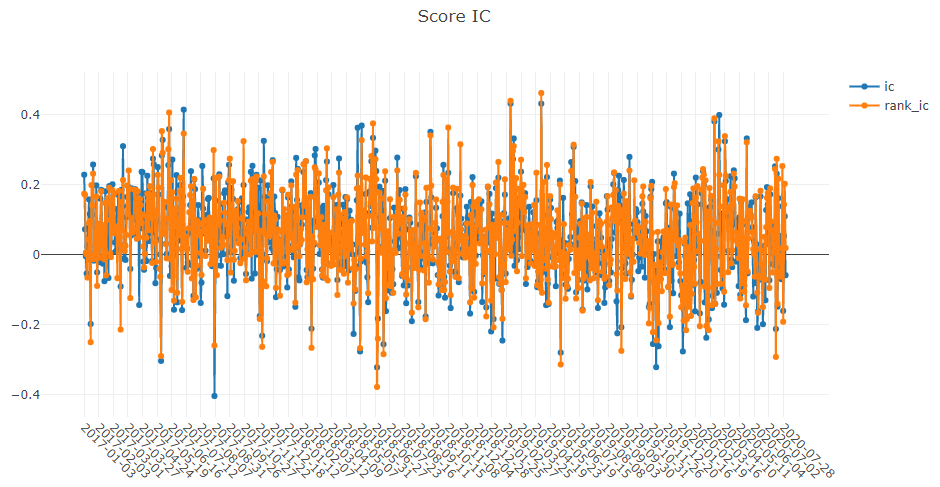

- qlib.contrib.report.analysis_position.score_ic.score_ic_graph(pred_label: DataFrame, show_notebook: bool = True, **kwargs) [<class 'list'>, <class 'tuple'>]

得分 IC

示例:

from qlib.data import D from qlib.contrib.report import analysis_position pred_df_dates = pred_df.index.get_level_values(level='datetime') features_df = D.features(D.instruments('csi500'), ['Ref($close, -2)/Ref($close, -1)-1'], pred_df_dates.min(), pred_df_dates.max()) features_df.columns = ['label'] pred_label = pd.concat([features_df, pred], axis=1, sort=True).reindex(features_df.index) analysis_position.score_ic_graph(pred_label)

- 参数:

pred_label -- 索引是 pd.MultiIndex,索引名称是 [instrument, datetime];列名称是 [score, label]。 .. code-block:: python instrument datetime score label SH600004 2017-12-11 -0.013502 -0.013502 2017-12-12 -0.072367 -0.072367 2017-12-13 -0.068605 -0.068605 2017-12-14 0.012440 0.012440 2017-12-15 -0.102778 -0.102778

show_notebook -- 是否在笔记本中显示图形,默认值为 True。

- 返回:

如果 show_notebook 为 True,则在笔记本中显示;否则返回 plotly.graph_objs.Figure 列表。

图形结果

备注

X轴:交易日

- Y轴:

- ic

标签与预测得分之间的`Pearson相关系数`系列。在上述示例中,label`被定义为`Ref($close, -2)/Ref($close, -1)-1。有关更多详细信息,请参阅`数据特征 <data.html#feature>`_。

- rank_ic

标签与预测得分之间的`Spearman等级相关系数`系列。

`analysis_position.risk_analysis`的使用

API

- qlib.contrib.report.analysis_position.risk_analysis.risk_analysis_graph(analysis_df: DataFrame | None = None, report_normal_df: DataFrame | None = None, report_long_short_df: DataFrame | None = None, show_notebook: bool = True) Iterable[Figure]

生成分析图和月度分析

示例:

import qlib import pandas as pd from qlib.utils.time import Freq from qlib.utils import flatten_dict from qlib.backtest import backtest, executor from qlib.contrib.evaluate import risk_analysis from qlib.contrib.strategy import TopkDropoutStrategy # init qlib qlib.init(provider_uri=<qlib data dir>) CSI300_BENCH = "SH000300" FREQ = "day" STRATEGY_CONFIG = { "topk": 50, "n_drop": 5, # pred_score, pd.Series "signal": pred_score, } EXECUTOR_CONFIG = { "time_per_step": "day", "generate_portfolio_metrics": True, } backtest_config = { "start_time": "2017-01-01", "end_time": "2020-08-01", "account": 100000000, "benchmark": CSI300_BENCH, "exchange_kwargs": { "freq": FREQ, "limit_threshold": 0.095, "deal_price": "close", "open_cost": 0.0005, "close_cost": 0.0015, "min_cost": 5, }, } # strategy object strategy_obj = TopkDropoutStrategy(**STRATEGY_CONFIG) # executor object executor_obj = executor.SimulatorExecutor(**EXECUTOR_CONFIG) # backtest portfolio_metric_dict, indicator_dict = backtest(executor=executor_obj, strategy=strategy_obj, **backtest_config) analysis_freq = "{0}{1}".format(*Freq.parse(FREQ)) # backtest info report_normal_df, positions_normal = portfolio_metric_dict.get(analysis_freq) analysis = dict() analysis["excess_return_without_cost"] = risk_analysis( report_normal_df["return"] - report_normal_df["bench"], freq=analysis_freq ) analysis["excess_return_with_cost"] = risk_analysis( report_normal_df["return"] - report_normal_df["bench"] - report_normal_df["cost"], freq=analysis_freq ) analysis_df = pd.concat(analysis) # type: pd.DataFrame analysis_position.risk_analysis_graph(analysis_df, report_normal_df)

- 参数:

analysis_df -- 分析数据,索引为 pd.MultiIndex;列名为 [risk]。 .. 代码块:: python risk excess_return_without_cost mean 0.000692 std 0.005374 annualized_return 0.174495 information_ratio 2.045576 max_drawdown -0.079103 excess_return_with_cost mean 0.000499 std 0.005372 annualized_return 0.125625 information_ratio 1.473152 max_drawdown -0.088263

report_normal_df -- df.index.name 必须为 date,df.columns 必须包含 return,turnover,cost,bench。 .. 代码块:: python return cost bench turnover date 2017-01-04 0.003421 0.000864 0.011693 0.576325 2017-01-05 0.000508 0.000447 0.000721 0.227882 2017-01-06 -0.003321 0.000212 -0.004322 0.102765 2017-01-09 0.006753 0.000212 0.006874 0.105864 2017-01-10 -0.000416 0.000440 -0.003350 0.208396

report_long_short_df -- df.index.name 必须为 date,df.columns 包含 long,short,long_short。 .. 代码块:: python long short long_short date 2017-01-04 -0.001360 0.001394 0.000034 2017-01-05 0.002456 0.000058 0.002514 2017-01-06 0.000120 0.002739 0.002859 2017-01-09 0.001436 0.001838 0.003273 2017-01-10 0.000824 -0.001944 -0.001120

show_notebook -- 是否在笔记本中显示图形,默认 True。如果为 True,则在笔记本中显示图形;如果为 False,则返回图形。

- 返回:

图形结果

备注

- 一般图形

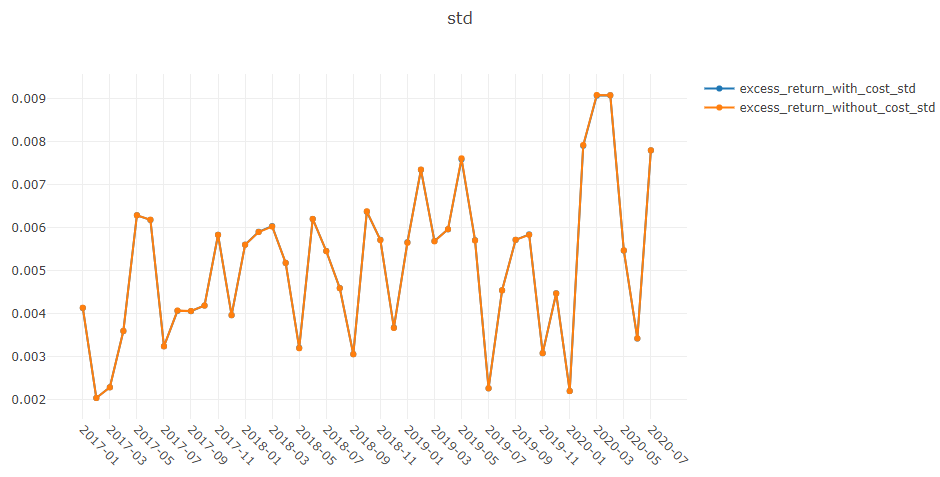

- 标准

- 不含成本的超额收益

不含成本的 CAR`(累积异常收益)的 `标准差。

- 含成本的超额收益

含成本的 CAR`(累积异常收益)的 `标准差。

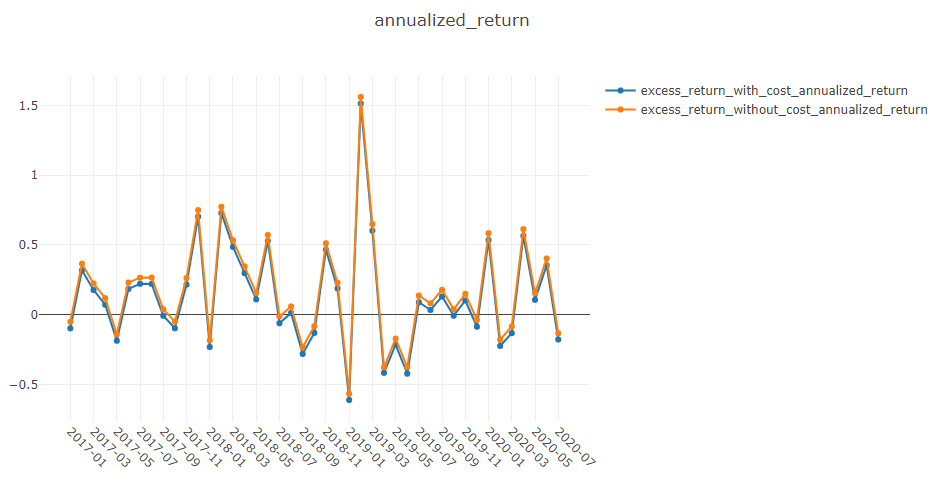

- 年化收益

- 不含成本的超额收益

不含成本的 CAR`(累积异常收益)的 `年化率。

- 含成本的超额收益

含成本的 CAR`(累积异常收益)的 `年化率。

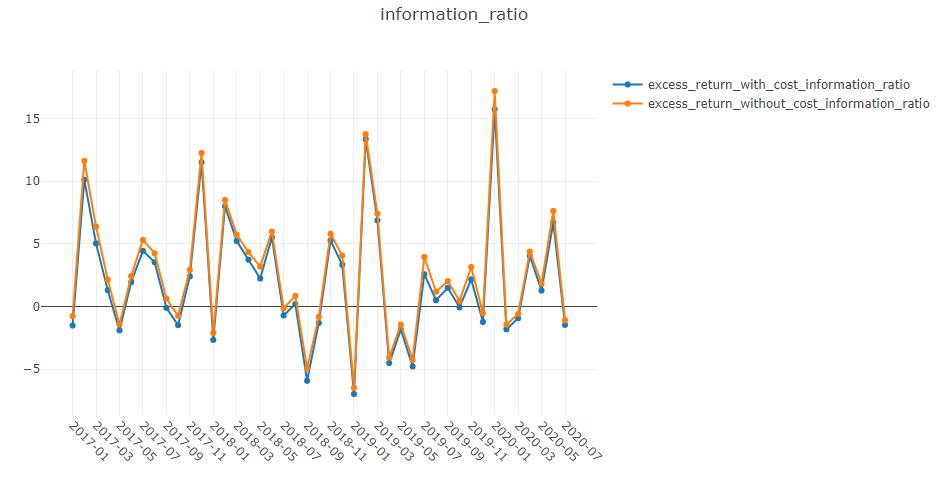

- 信息比率

- 不含成本的超额收益

不含成本的 信息比率。

- 含成本的超额收益

含成本的 信息比率。

要了解更多关于 信息比率 的信息,请参考 信息比率 – IR。

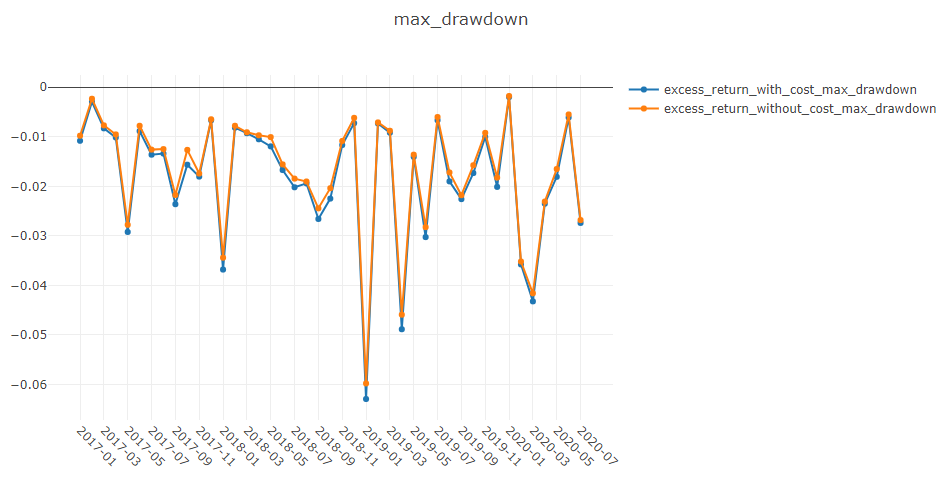

- 最大回撤

- 不含成本的超额收益

不含成本的 CAR`(累积异常收益)的 `最大回撤。

- 含成本的超额收益

含成本的 CAR`(累积异常收益)的 `最大回撤。

备注

- 年化收益/最大回撤/信息比率/标准图形

X轴:按月分组的交易日

- Y轴:

- 年化收益图形

- 不含成本的超额收益年化收益

无成本的每月 CAR`(累积异常收益)的 `年化收益率 系列。

- excess_return_with_cost_annualized_return

有成本的每月 CAR`(累积异常收益)的 `年化收益率 系列。

- 最大回撤图形

- excess_return_without_cost_max_drawdown

无成本的每月 CAR`(累积异常收益)的 `最大回撤 系列。

- excess_return_with_cost_max_drawdown

有成本的每月 CAR`(累积异常收益)的 `最大回撤 系列。

- 信息比率图形

- excess_return_without_cost_information_ratio

无成本的每月 CAR`(累积异常收益)的 `信息比率 系列。

- excess_return_with_cost_information_ratio

有成本的每月 CAR`(累积异常收益)的 `信息比率 系列。

- 标准差图形

- excess_return_without_cost_max_drawdown

无成本的每月 CAR`(累积异常收益)的 `标准差 系列。

- excess_return_with_cost_max_drawdown

有成本的每月 CAR`(累积异常收益)的 `标准差 系列。

analysis_model.analysis_model_performance 的使用

API

- qlib.contrib.report.analysis_model.analysis_model_performance.ic_figure(ic_df: DataFrame, show_nature_day=True, **kwargs) Figure

IC 图

- 参数:

ic_df -- ic 数据框

show_nature_day -- 是否显示非交易日的横坐标

**kwargs -- 包含一些参数以控制 plotly 中的绘图样式。目前支持 - rangebreaks: https://plotly.com/python/time-series/#Hiding-Weekends-and-Holidays

- 返回:

plotly.graph_objs.Figure

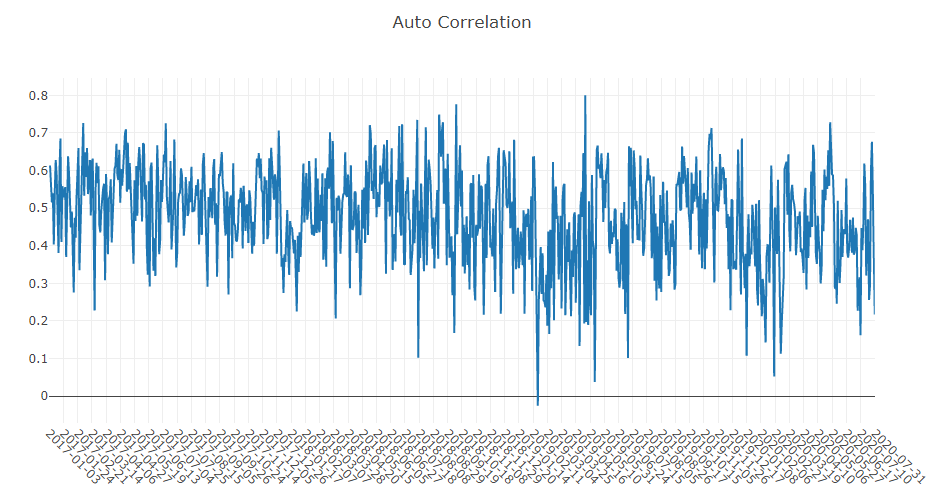

- qlib.contrib.report.analysis_model.analysis_model_performance.model_performance_graph(pred_label: DataFrame, lag: int = 1, N: int = 5, reverse=False, rank=False, graph_names: list = ['group_return', 'pred_ic', 'pred_autocorr'], show_notebook: bool = True, show_nature_day: bool = False, **kwargs) [<class 'list'>, <class 'tuple'>]

模型性能

- 参数:

pred_label -- 索引是 pd.MultiIndex,索引名称是 [instrument, datetime];列名称是 [score, label]。它通常与模型训练的标签相同(例如:"Ref($close, -2)/Ref($close, -1) - 1")。 .. code-block:: python instrument datetime score label SH600004 2017-12-11 -0.013502 -0.013502 2017-12-12 -0.072367 -0.072367 2017-12-13 -0.068605 -0.068605 2017-12-14 0.012440 0.012440 2017-12-15 -0.102778 -0.102778

lag -- pred.groupby(level='instrument')['score'].shift(lag)。它将仅用于自相关计算。

N -- 组数,默认值为 5。

reverse -- 如果 True,则 pred['score'] *= -1。

rank -- 如果 True,计算排名 ic。

graph_names -- 图形名称;默认值 ['cumulative_return', 'pred_ic', 'pred_autocorr', 'pred_turnover']。

show_notebook -- 是否在笔记本中显示图形,默认值为 True。

show_nature_day -- 是否显示非交易日的横坐标。

**kwargs -- 包含一些参数以控制 plotly 中的绘图样式。目前支持 - rangebreaks: https://plotly.com/python/time-series/#Hiding-Weekends-and-Holidays

- 返回:

如果 show_notebook 为 True,则在笔记本中显示;否则返回 plotly.graph_objs.Figure 列表。

图形结果

备注

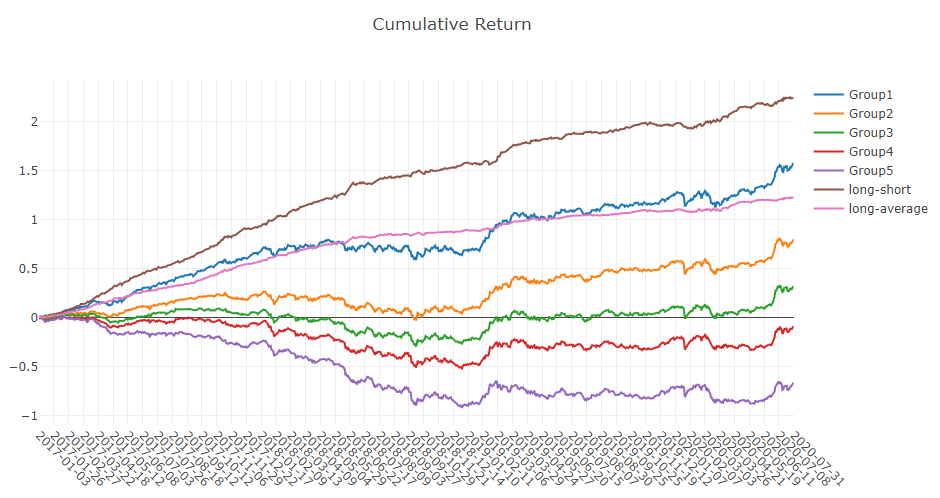

- 累积收益图形

- Group1:

标签排名比例 <= 20% 的股票组的 累计收益 系列

- 组2:

标签排名比例在 20% < 标签排名比例 <= 40% 的股票组的 累计收益 系列

- 组3:

标签排名比例在 40% < 标签排名比例 <= 60% 的股票组的 累计收益 系列

- 组4:

标签排名比例在 60% < 标签排名比例 <= 80% 的股票组的 累计收益 系列

- 组5:

标签排名比例在 80% < 标签排名比例 的股票组的 累计收益 系列

- 多空:

组1 和 组5 的 累计收益 之间的差异系列

- 多平均

组1 的 累计收益 和所有股票的平均 累计收益 之间的差异系列。

- 标签排名比例可以如下公式表示。

- \[排名\ 比例 = \frac{标签的升序排名}{投资组合中的股票数量}\]

备注

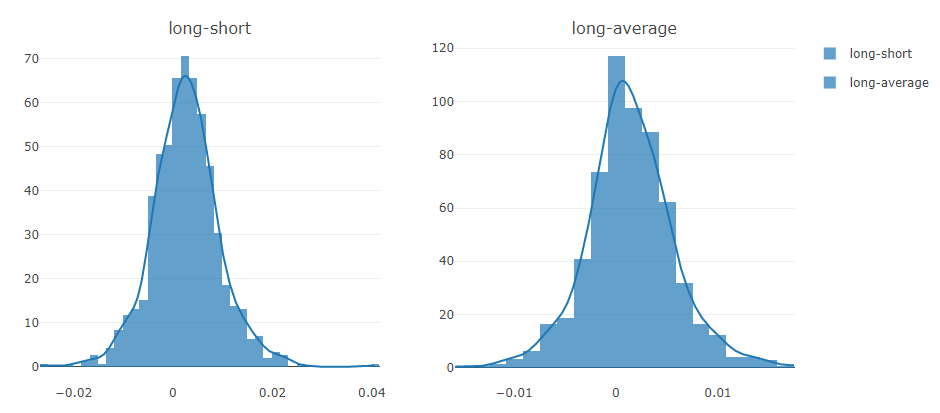

- 多空/多平均

每个交易日的多空/多平均收益的分布

备注

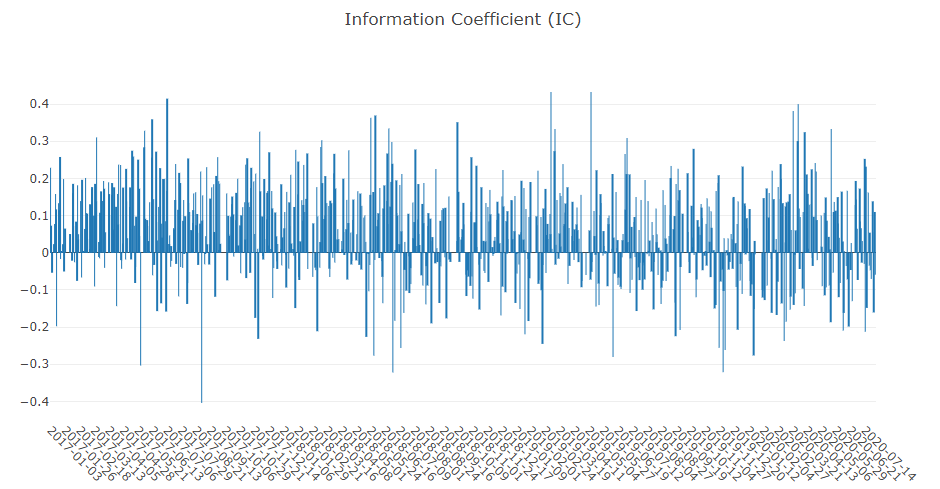

- 信息系数

投资组合中股票的 标签 和 预测分数 之间的 皮尔逊相关系数 系列。

图形报告可用于评估 预测分数。

备注

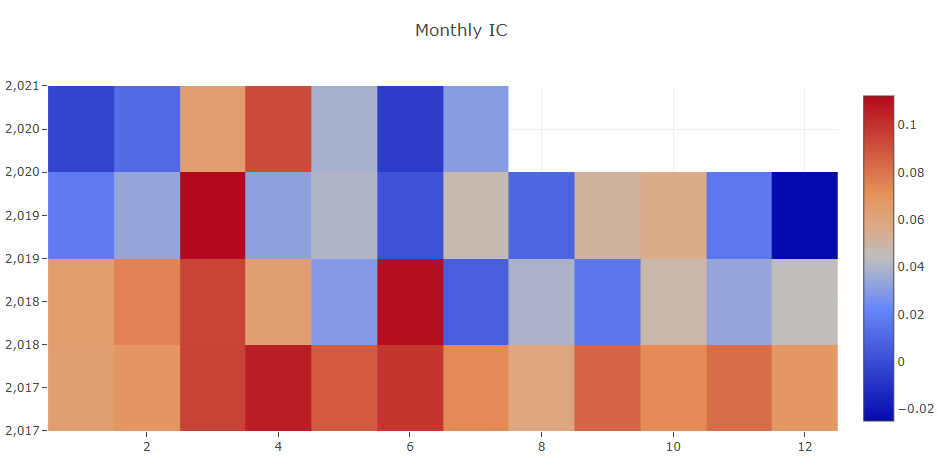

- 每月 IC

每月 信息系数 的平均值

备注

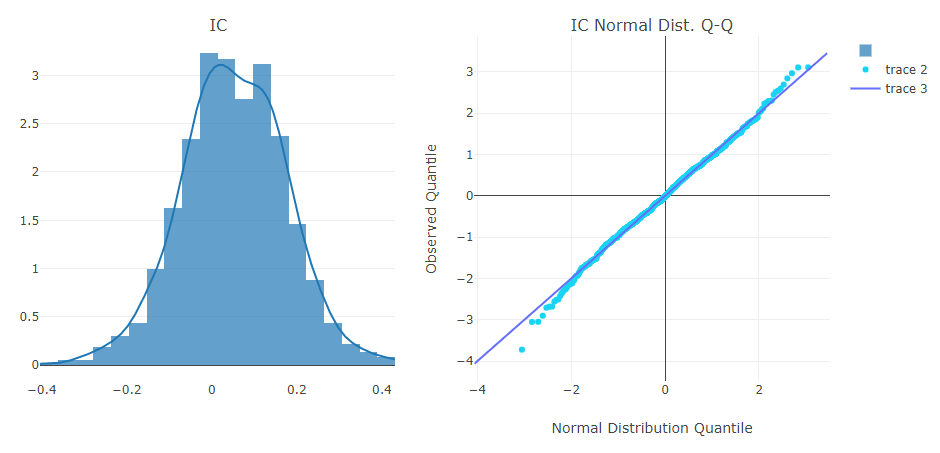

- IC

每个交易日的 信息系数 分布。

- IC 正态分布 Q-Q

分位数-分位数图 用于每个交易日的 信息系数 的正态分布。

备注

- 自相关

每个交易日投资组合中股票最新的 预测分数 与 滞后 天前的 预测分数 之间的 皮尔逊相关系数 序列。

图形报告可用于估计换手率。